When locking in profits makes sense — and when it costs you.

TL;DR:

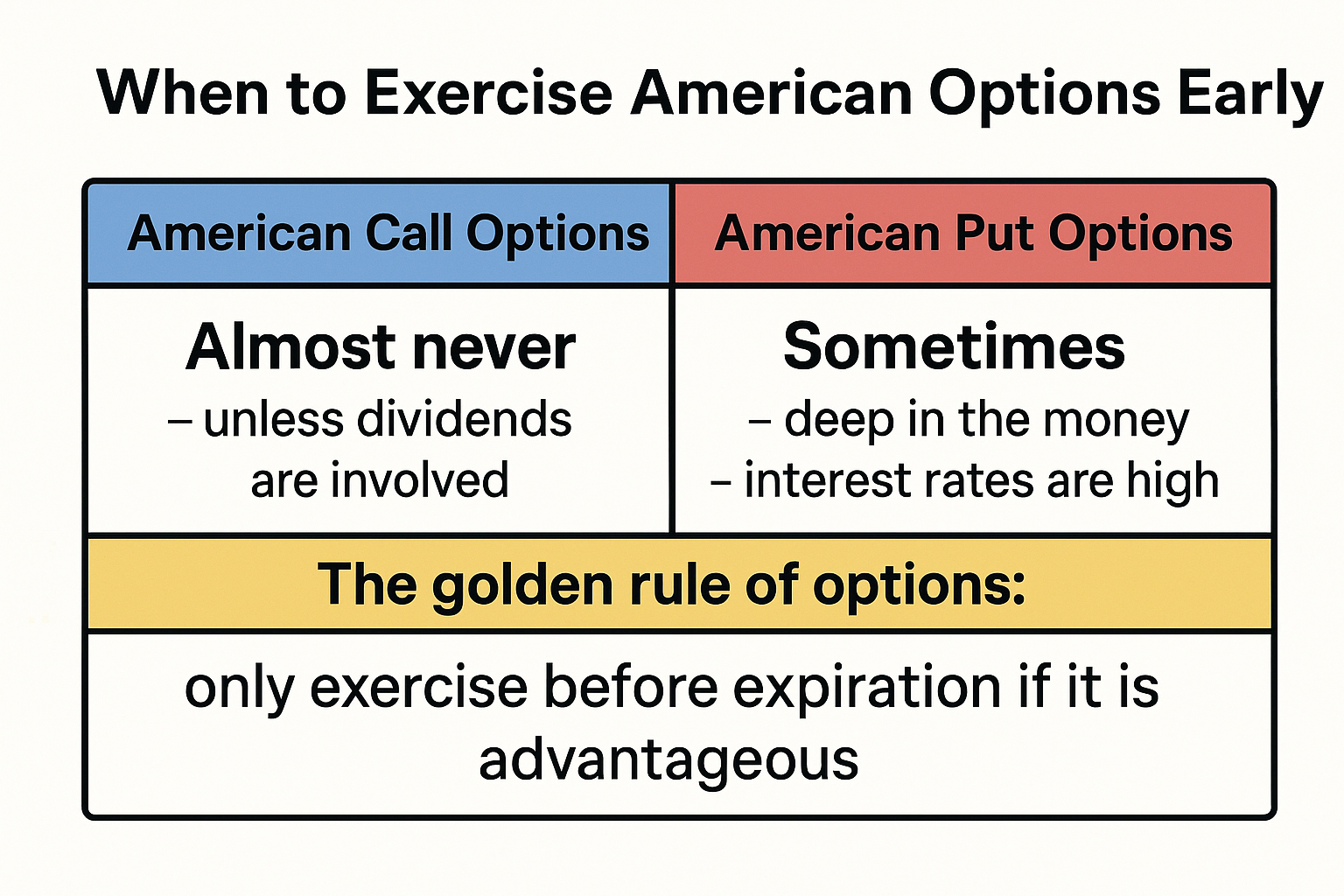

- American call options: Almost never worth exercising early — unless dividends are involved.

- American put options: Sometimes yes — especially when deep in the money or interest rates are high.

- This post walks you through when and why early exercise makes sense, backed by code and charts.

What Does “Early Exercise” Even Mean?

American options give you the flexibility to exercise at any time before or at expiration.

That means:

- You can buy (call) or sell (put) the underlying asset early, instead of waiting until expiry.

But just because you can doesn’t mean you should.

The golden rule of options:

Never exercise early unless the payoff exceeds the time value you’re giving up.

You should almost never exercise an American option early, except in specific situations—primarily for certain puts or for calls right before a significant dividend is paid. Exercising most American options early results in the loss of remaining time value, making it economically suboptimal in most scenarios.

American Call Options: Is Early Exercise Ever Optimal?

❌ In general: No.

Let’s say you hold an American call option on a stock with:

- No dividends

- Time left until expiry

- Price above the strike

You might think: “Why not just exercise now and take the profit?”

Bad idea. Here’s why:

Holding the option is better because:

- You still have unlimited upside if the stock goes higher

- You delay paying the strike price

- You can sell the option instead and capture the same intrinsic value plus time value

Exception: Dividends

Early exercise of an American call option is generally not optimal if the underlying stock does not pay dividends. This is because holding the option preserves both its time value and flexibility; exercising early forfeits this time value and causes you to pay the strike price sooner, losing potential interest. An exception exists if the stock is about to pay a dividend. In that case, exercising right before the ex-dividend date may make sense, as it allows the investor to capture the dividend. Even then, only deep in-the-money calls are likely to qualify.

So if the stock pays a dividend before expiration, it might be optimal to exercise the day before the ex-dividend date — because:

- Option holders don’t receive dividends

- Shareholders do

- So exercising early may help capture that dividend payout

Summary:

| Call Option on… | Early Exercise Optimal? |

|---|---|

| Non-dividend-paying stock | ❌ No |

| Dividend-paying stock | ✅ Possibly (before ex-dividend) |

American Put Options: When Is Early Exercise Optimal?

✅ Sometimes yes — especially when deep in the money

Puts give you the right to sell at a fixed price. If the stock plummets, you can lock in a guaranteed sale price.For American put options, early exercise might be advantageous if the option is deep in the money, interest rates are high, and the present value of the strike price (received on exercise) earns more than the remaining option time value. This is more likely when you want to sell the underlying stock, receive the strike price early, and invest that money sooner.

If you wait, the time value might not outweigh the guaranteed payoff.

🧠 Scenarios where early exercise makes sense:

- The put is deep in the money (stock ≪ strike)

- There’s little time left until expiration

- Interest rates are high, so money now is better than later

Most traders, however, will usually realize more profit by selling the option in the market than by exercising it early, since the price includes both intrinsic and time value. Early exercise only makes sense when the additional benefit (such as dividend receipt or interest earned from immediate exercise of a deep-in-the-money put) outweighs the lost time value.

Remember: early exercise on puts is about locking in certainty when there’s little value left in waiting.

In summary, early exercise of American options is rarely optimal for non-dividend-paying calls and is only occasionally optimal for deep-in-the-money puts or dividend-paying stocks—situations requiring careful value comparisons.

Visual Comparison (Code-Backed)

Below is a chart generated using Python. It compares:

- The Black-Scholes value of a European call and put

- The intrinsic value (immediate exercise value)

You’ll see:

- For calls, the Black-Scholes price is always higher than intrinsic (early exercise = bad).

- For puts, when the stock price is low, intrinsic value can exceed Black-Scholes price (early exercise = good).

Python Code (for readers & quants)

Here’s a simplified Python script to recreate the chart:

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

# Parameters

K = 100

r = 0.05

T = 1

sigma = 0.25

S = np.linspace(1, 200, 500)

# Black-Scholes European Call and Put

def call_price(S, K, r, T, sigma):

d1 = (np.log(S/K) + (r + 0.5*sigma**2)*T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

return S * norm.cdf(d1) - K * np.exp(-r*T) * norm.cdf(d2)

def put_price(S, K, r, T, sigma):

d1 = (np.log(S/K) + (r + 0.5*sigma**2)*T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

return K * np.exp(-r*T) * norm.cdf(-d2) - S * norm.cdf(-d1)

# Intrinsic values

intrinsic_call = np.maximum(S - K, 0)

intrinsic_put = np.maximum(K - S, 0)

# Plotting

plt.figure(figsize=(10, 6))

plt.plot(S, call_price(S, K, r, T, sigma), label='European Call Price')

plt.plot(S, intrinsic_call, '--', label='Call Intrinsic Value')

plt.plot(S, put_price(S, K, r, T, sigma), label='European Put Price')

plt.plot(S, intrinsic_put, '--', label='Put Intrinsic Value')

plt.axvline(K, color='gray', linestyle=':', label='Strike Price (K)')

plt.title('Early Exercise: Call vs Put Option Logic')

plt.xlabel('Stock Price ($)')

plt.ylabel('Option Value ($)')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

In summary, early exercise of American options is rarely optimal for non-dividend-paying calls and is only occasionally optimal for deep-in-the-money puts or dividend-paying stocks—situations requiring careful value comparisons.