If you told me a few years ago that I’d be spending my mornings coding trading algorithms and my evenings studying market theory, I might have laughed. For most of my career, my world was Mechanics of material, Structural Analysis and the kind of math that keeps bridges standing and skyscrapers safe.

I earned my PhD in Civil and Infrastructure Engineering, specializing in smart structures and digital twin technology— systems that use sensors, real-time data, and computational models to monitor and predict structural performance. Along the way, I mastered the mathematical and computational foundations that make both engineering and finance possible: advanced linear algebra, nonlinear finite element analysis, statistics, probability theory, computational mathematics, and numerical methods. These tools weren’t just academic — I applied them to model complex, dynamic systems under uncertainty, a skill set that now gives me a deep edge in quantitative finance and algorithmic trading.

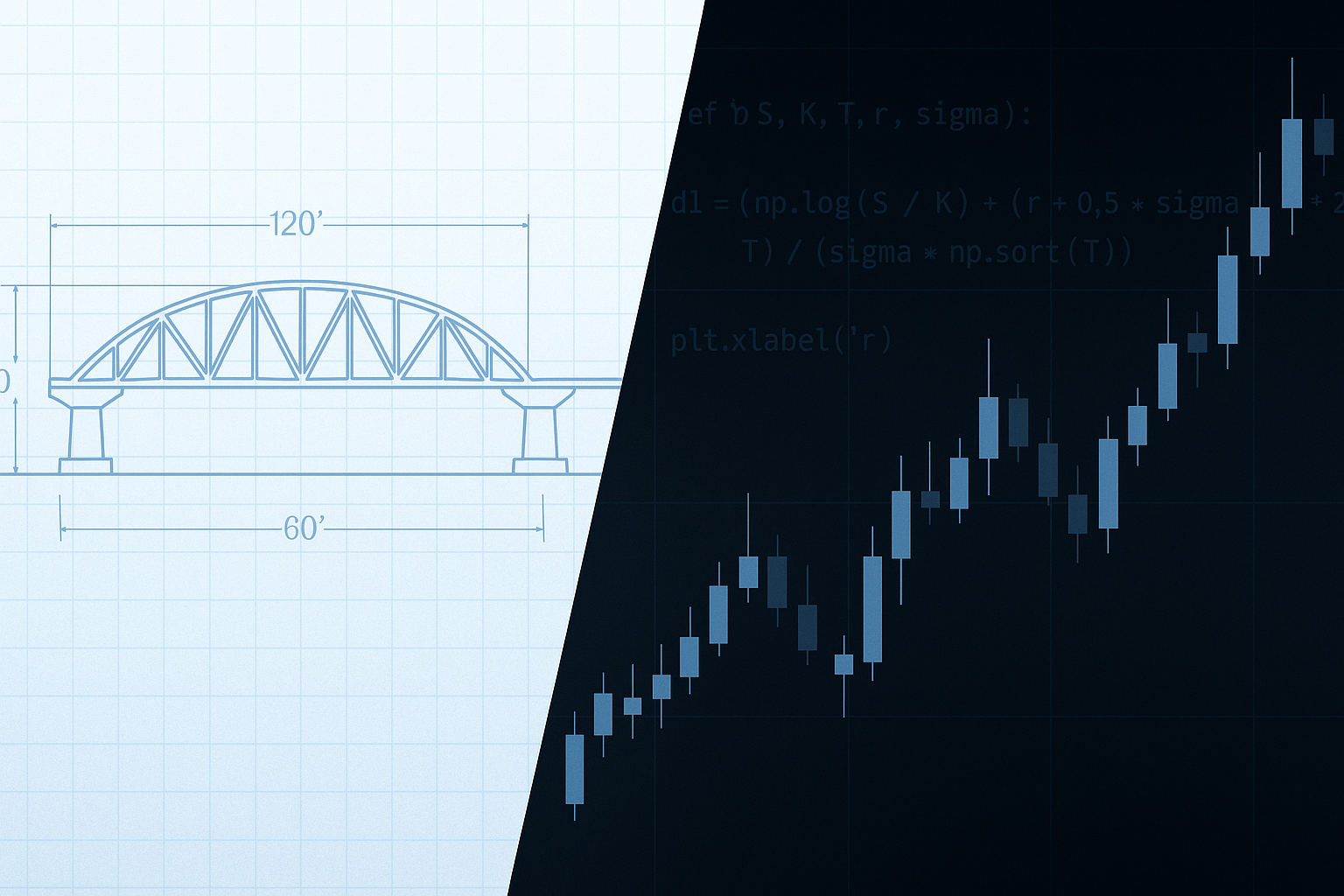

But here’s the thing: markets are systems too.

How the shift began

I’ve always had an interest in finance, but my real turning point came when I started actively trading the U.S. markets. I wasn’t just buying and selling stocks — I was testing strategies, tracking performance, and learning how market behavior changes under different conditions. I traded through volatile periods, learned from wins and losses, and realized something important: the same analytical mindset I used in engineering could be applied to markets.

When I looked at a price chart, I saw more than just numbers. I saw patterns, stress points, and the “load” the market was carrying. It reminded me of structural analysis — only here, the forces were driven by human behavior, macroeconomic events, and algorithms.

Going all in on learning

Once I saw the parallels, I couldn’t unsee them. I dove into quantitative finance headfirst — studying Robert Shiller’s Financial Markets course, John Geanakoplos’s Financial Theory, stochastic calculus, probability theory, and market microstructure.

I started building Python models for options pricing, backtesting strategies like moving average crossovers and mean reversion, running Monte Carlo simulations, and calculating portfolio risk metrics. I experimented with my own trading algorithms in the U.S. equity market, tracking not only returns but volatility and drawdowns.

The deeper I went, the more I realized this wasn’t a hobby anymore — this was the next chapter of my career.

Why this matters for Gilanar Analytics

Gilanar Analytics is my way of bridging two worlds: the engineering precision I’ve honed over years, and the financial modeling skills I’ve developed through study and hands-on trading. My goal isn’t just to build models that work on paper, but to design strategies and tools that can survive real market conditions — just like a good bridge can survive wind, rain, and traffic.

I believe in sharing what I learn, testing ideas openly, and improving through iteration. My approach is analytical, but also human — because at the heart of every market move are people making decisions.

This journey from engineering to trading to quantitative research has been challenging, humbling, and exciting. And I’m just getting started.

If you’ve ever wondered how engineering logic can meet financial innovation, or if you’re curious about how data can be turned into trading decisions, you’re in the right place.

Welcome to Gilanar Analytics. Let’s build something that lasts.